Skip to content

Skip to content

Embark on a financial odyssey as we dissect the intricate dance between Accounts Payable and Accounts Receivable in 5 illuminating points. Unleash your financial acumen and sculpt a success story uniquely yours in the vibrant landscape of fiscal dynamics.

Embarking on the enchanting journey through the intricate labyrinth of corporate finance, we find ourselves in the midst of a grand ballet—one choreographed by the delicate interplay between two central figures, Accounts Payable (AP) and Accounts Receivable (AR). In this narrative odyssey, we unravel the mystique surrounding Account Payable versus Accounts Receivable, peeling back layers to reveal not only their nuanced functions but also their profound significance in the dance of financial management.

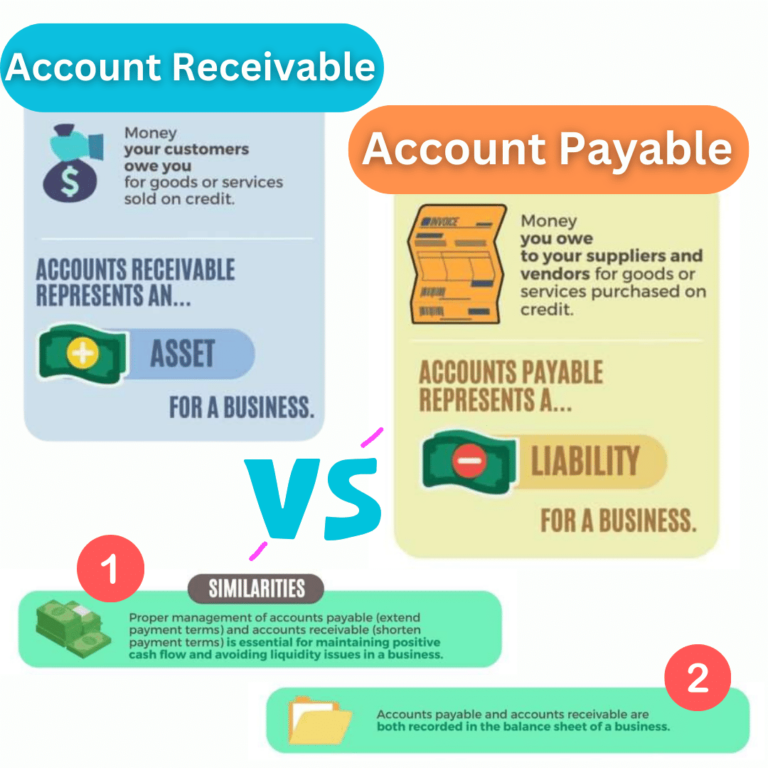

Enter the first protagonist, Accounts Payable (AP), draped in the robes of financial obligation. AP embodies the promises whispered by a business to its suppliers and vendors, promises awaiting fulfillment for goods and services already enjoyed. It is a liability, a dance partner whose every step is recorded meticulously on the company’s balance sheet, a rhythmic manifestation of debts to be settled within the harmonious cadence of agreed-upon temporal bounds.

Accounts Payable, beyond its ledger entries, is the custodian of short-term debts, a keeper of financial promises. It is the curator of a delicate waltz, where maintaining the tempo of invoices, payment terms, and due dates is not merely a routine but a performance critical to the orchestra’s harmony. Failure to honor these financial commitments casts shadows on the stage—strained relationships with suppliers, late payment penalties, and a dissonance in the company’s credit symphony.

In the spotlight, we introduce the second dancer, Accounts Receivable (AR), bedecked in the jewels of anticipated wealth. AR is the financial echo of credit extended by the company to its patrons, a tangible testament to the virtuosity of goods and services rendered. As a current asset adorning the balance sheet, AR beckons, embodying the anticipation of cash inflows pirouetting within a specified timeframe.

AR management, akin to a pas de deux, requires strategic choreography—credit policies are the opening movements, invoicing procedures the graceful twirls, and vigilant follow-ups on overdue payments the dramatic leaps. The swift collection of receivables orchestrates a symphony of liquidity, ensuring a seamless flow, an unbroken rhythm of operational fluidity.

In this grand ballet, distinctions between the leading characters are not just footnotes but entire movements. Let’s appreciate the nuanced choreography:

Nature of Transaction:

– Accounts Payable is the company’s partner in financial liabilities to external entities.

– Accounts Receivable, a soloist, embodies the company’s financial assets—a testament to funds owed by external counterparts.

Direction of Cash Flow:

– Accounts Payable’s choreography demands a graceful cash outflow during the settlement of outstanding obligations.

– Accounts Receivable, the maestro, conducts a cash-in symphony when customers gracefully fulfill their financial commitments.

Timing of Transactions:

– Accounts Payable is a retrospective dance, a consequence of expenses already incurred.

– Accounts Receivable’s dance is an anticipation, tethered to recognized revenue yet awaiting its moment of realization.

Role in Working Capital Dynamics:

– Accounts Payable adds depth to the canvas of short-term liabilities.

– Accounts Receivable, an aerialist, interlaces with short-term assets, shaping the dynamic contours of working capital.

As the kaleidoscope of corporate finance continues its mesmerizing whirl, the mastery of the dance between Accounts Payable and Accounts Receivable transcends the mundane. It becomes an art form, an intricate ballet of liquidity, working capital, and cash flow. Through the adoption of advanced strategies, the embrace of technological prowess, and the nurturing of transparent communication with stakeholders, businesses not only find equilibrium in the duet of payables and receivables but also forge a path towards enduring success.

In the ever-evolving ballet of business, the imperative for a profound comprehension of the dance between Accounts Payable and Accounts Receivable becomes non-negotiable. The cultivation of financial discipline, coupled with the assimilation of best practices, positions organizations at the vanguard of financial stewardship. Here, in this grand ballet, they stand—poised for enduring success in a realm characterized by unrelenting dynamism, an ever-changing stage upon which the dance of competition unfolds.

Accounts Payable, or AP, plays a central role in managing the financial obligations a business owes to its suppliers and vendors for goods and services received. It is a meticulous record-keeping system that tracks outstanding amounts, ensuring timely settlement within agreed-upon timeframes.

Accounts Payable is instrumental in managing short-term debts. By maintaining accurate records of invoices, payment terms, and due dates, Accounts Payable ensures the timely settlement of financial commitments. This not only fosters healthy relationships with suppliers but also avoids penalties and safeguards the company's creditworthiness.

Accounts Receivable represents the money owed to a business by its customers for goods or services rendered. As a current asset on the balance sheet, AR symbolizes anticipated cash inflows within a specified period. AR management is crucial for optimizing liquidity, ensuring a steady cash flow, and sustaining operational fluidity.

Efficient management of Accounts Receivable involves strategic credit policies, seamless invoicing procedures, and vigilant follow-ups on overdue payments. Swift collections from customers contribute to financial stability, enhance liquidity, and ensure uninterrupted operational flow.

The distinctions between Accounts Payable and Accounts Receivable are multifaceted:

- Accounts Payable involves the company's financial liabilities to external entities, while Accounts Receivable represents the company's financial assets.

- Accounts Payable leads to cash outflow during settlement, whereas Accounts Receivable results in cash inflow when customers fulfill their financial commitments.

- Accounts Payable is associated with expenses already incurred, while Accounts Receivable is tied to recognized revenue yet to be realized.

- Accounts Payable contributes to short-term liabilities, while Accounts Receivable influences short-term assets, shaping working capital dynamics.

Accounts Payable and Accounts Receivable play pivotal roles in optimizing working capital. Balancing the timing of payments to suppliers (AP) and the collection of receivables (AR) ensures a healthy cash flow, fostering a resilient and robust working capital environment.

Timely settlements through Accounts Payable nurture trust with suppliers, while effective credit policies, transparent communication, and prompt collections through Accounts Receivable cultivate enduring relationships with customers. This harmonious interplay enhances the overall financial ecosystem.

Accounts Payable and Accounts Receivable data serve as the foundation for financial planning and analysis. These metrics offer valuable insights for informed decision-making in budgeting, resource allocation, and overall financial strategy, empowering financial custodians with a data-driven approach.

Cutting-edge automation technologies streamline Accounts Payable and Accounts Receivable processes, reducing errors and enhancing operational efficiency. Automation facilitates seamless invoice processing, payment scheduling, and receivables tracking, contributing to the overall effectiveness of financial management.

Strategies include:

- Leveraging technological ascendancy through automation.

- Engaging in negotiation finesse for favorable payment terms.

- Implementing vigilant monitoring and strategic reporting of Accounts Payable and Accounts Receivable metrics.

- Conducting thorough credit proficiency exercises for risk mitigation.

The balletic analogy infuses creativity into the understanding of Accounts Payable and Accounts Receivable dynamics. It highlights the nuanced choreography, distinctions, and strategic significance of these financial elements, turning the complex into an artistic narrative for a more engaging comprehension.

Explore the dynamic world of Accounting and Finance with insights from a seasoned professional. As an ACCA and MS Accounting & Finance graduate, I bring expertise to FinanceAccounting.us, offering valuable perspectives and practical tips for navigating the intricate realms of financial management and accounting

Explore the intricate realms of finance and accounting with me, and let’s embark on a journey to enhance your financial prowess. Whether you seek strategic financial guidance or comprehensive accounting knowledge, I am here to empower you

All Rights Reserved © 2024 FinanceAccounting.US | Privacy Policy

Optimized by Seraphinite Accelerator

Optimized by Seraphinite Accelerator